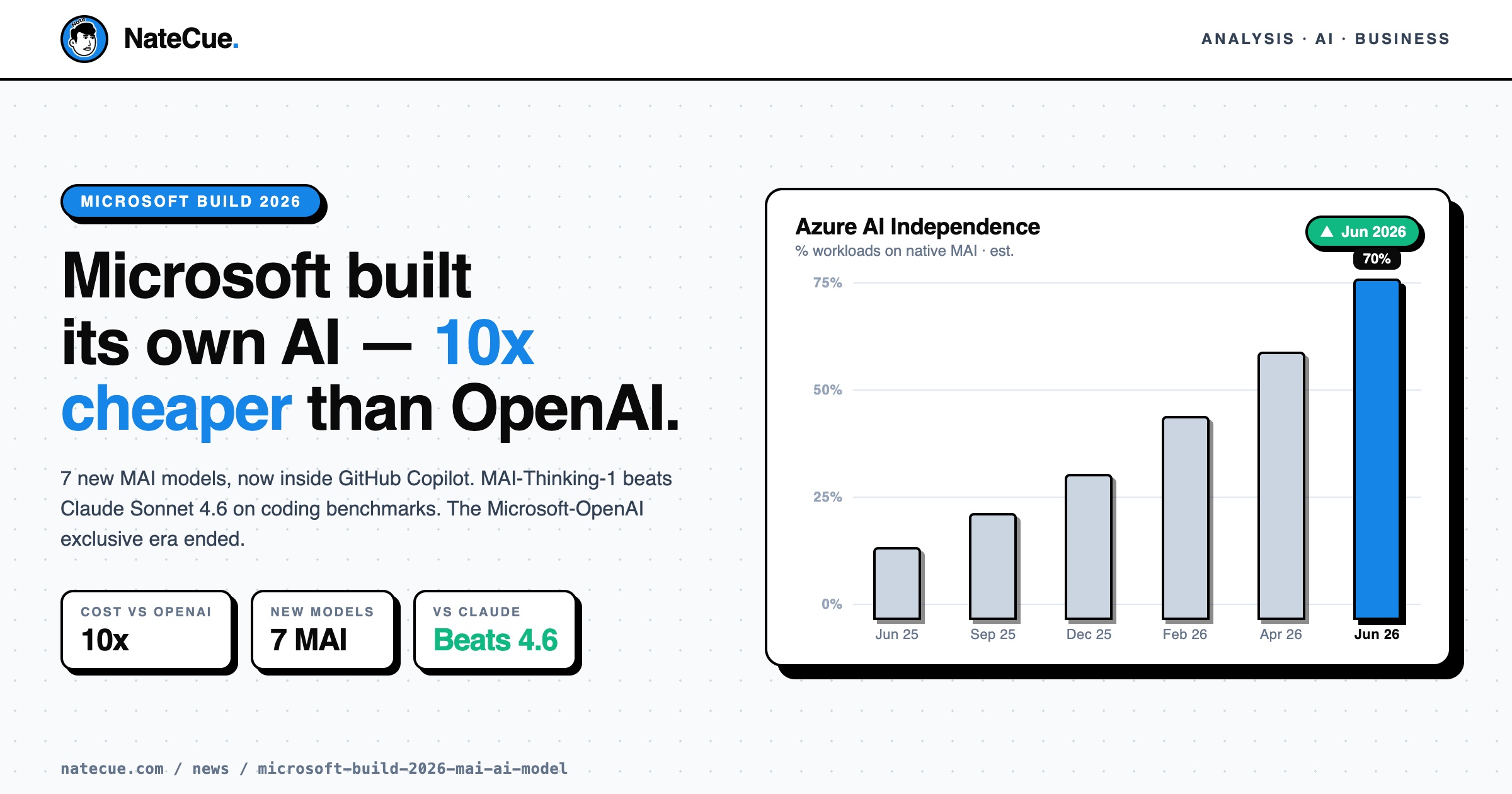

Microsoft is OpenAI’s largest investor. This week, they launched seven in-house AI models to make that relationship optional.

At Build 2026 (June 2-3), Microsoft unveiled the MAI family - seven proprietary models spanning reasoning, coding, image generation, transcription and voice. Mustafa Suleiman, Microsoft AI CEO, put the cost advantage plainly: MAI delivers OpenAI-level performance at one-tenth the cost. And one of those models is already running inside GitHub Copilot.

What Microsoft Shipped at Build 2026

MAI-Thinking-1 is the flagship: a 35-billion-active-parameter reasoning model with a 256K token context window, trained entirely without OpenAI data. On SWE-Bench Pro - the most widely used coding benchmark in the industry - MAI-Thinking-1 beats Claude Sonnet 4.6 and matches Claude Opus 4.6 (IndexBox, 2026). That’s not a tier-2 model trying to be relevant. That’s frontier performance from a model Microsoft built itself.

MAI-Code-1-Flash is already inside GitHub Copilot and VS Code. If you used GitHub Copilot today, you used MAI - not GPT.

MAI-Image-2.5 handles text-to-image and image-to-image workflows, currently ranked top 3 on the AI Arena leaderboard for visual generation.

MAI-Transcribe-1.5 delivers high-accuracy speech-to-text across 43 languages.

MAI-Voice-2 and its Flash variant add 15+ new languages to voice synthesis.

All seven models are available on Azure, Fireworks AI, Baseten, and Open Router.

Why Now - And Why the Business Logic Is Airtight

In April 2026, Microsoft and OpenAI amended their partnership agreement: Microsoft gave up its exclusive right to market and distribute OpenAI models. A non-exclusive arrangement runs through 2032, but the exclusivity is gone.

The financial logic is transparent: every Azure customer query running on OpenAI API means royalty payments flowing to OpenAI. By running MAI on Microsoft’s own infrastructure, those royalty costs disappear entirely. A 10x cost reduction isn’t a margin improvement - it’s a structural rebuild of the cost stack.

Microsoft now holds a position unprecedented in tech history:

- Largest investor in OpenAI

- Direct competitor to OpenAI (via MAI)

- Largest customer of OpenAI (Azure still hosts GPT models)

These three roles are structurally incompatible at scale. Build 2026 is the first public signal of which direction that tension resolves.

What This Means for Enterprises and Developers

Most Microsoft 365 Copilot users don’t know which AI model is running behind the interface. They see “Copilot.” After Build 2026, that could be MAI-Thinking-1, GPT-4o, or a mix - routed by Microsoft without notice.

For enterprises on Azure:

AI pricing pressure is moving in the right direction. Without OpenAI royalties embedded in Azure’s cost structure, compute costs for AI workloads should decrease over time. For high-volume Azure AI workloads, this is a positive structural development for long-term budgets.

The risk: applications built on specific OpenAI model behaviors may see silent routing changes. If you’ve built assumptions about response format, behavior, or edge cases based on GPT - verify those against MAI before they become production surprises.

For developers on GitHub Copilot:

MAI-Code-1-Flash’s benchmark numbers are strong. But SWE-Bench measures code completion accuracy on standardized tasks - not the texture of inline suggestions during complex multi-file refactors. Test against your actual workflows before assuming benchmark equals experience.

For founders building AI strategy:

“Microsoft” and “OpenAI” are no longer synonyms. If your stack depends on OpenAI capabilities routed through Azure, you need to know whether you’re hitting the OpenAI endpoint or the MAI endpoint. Different pricing, different rate limits, potentially different behavior on edge cases.

The Vietnam Angle: Where the Price Gap Forces Real Decisions

Vietnam’s enterprise market is Microsoft-first and cost-sensitive. Azure is the dominant cloud platform for mid-market Vietnamese companies. Microsoft 365 is standard office infrastructure.

When a CTO needs to justify AI budget to a board, a 10x cost differential on inference is not a theoretical number - it’s a procurement conversation. Vietnam is likely one of the first APAC markets where MAI’s cost advantage creates real switching pressure, precisely because cost discipline in enterprise procurement is high and brand loyalty to “OpenAI specifically” - as opposed to AI tools generally - is lower than in US markets.

The Bigger Picture: AI Stack Fragmentation Is Here

Build 2026 is the clearest signal yet that the era of “pick one AI provider and you’re done” is over.

Google has Gemini. Anthropic has Claude. OpenAI has GPT-5. Microsoft has MAI. Meta has Llama (open source). Every major provider is building a full stack - models, infrastructure, applications. The consolidation of 2023-2024 is giving way to the fragmentation of 2025-2026.

For businesses building AI into operations now: lock in on use cases and outcomes, not on specific model names. The model running your workflow in Q3 may not be the one running it in Q1 2027. The market is moving faster than any enterprise procurement cycle.

NateCue's Take

The story everyone is missing: OpenAI is being squeezed on every flank simultaneously. Google has Gemini. Meta has Llama (open source). Microsoft now has MAI. Every major enterprise platform has an alternative. OpenAI's remaining moat is brand - ChatGPT is still the consumer default. But brand doesn't win enterprise procurement. When Microsoft can offer 10x cheaper inference on Azure with frontier-adjacent performance, CTO justifications for premium OpenAI pricing become arguments about name recognition, not capability. OpenAI needs to accelerate its consumer business faster than it currently is - before the enterprise segment is systematically undercut from every direction. For Vietnam specifically: this price delta lands in a market where cost discipline matters more than brand loyalty. The migration timeline is shorter than most expect.