Every agency now has access to GPT-5. Every agency can spin up a Claude-powered agent. So where does competitive advantage in advertising actually come from?

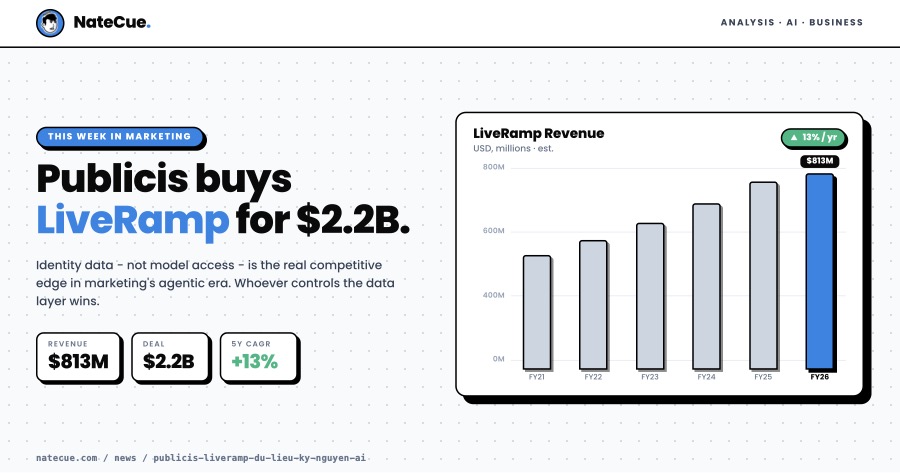

On May 17, 2026, Publicis Groupe answered that question with a $2.2 billion check written to LiveRamp.

What LiveRamp Actually Is (and Why It Matters)

LiveRamp isn’t an agency or a media platform. It’s identity infrastructure - the connective tissue linking user data across 25,000 publisher domains, 500+ data partners in 14 markets, serving 800 clients including 250 Fortune 500 companies (Digiday, 2026).

Its core product, RampID, functions as the industry’s shared currency for matching user data across platforms in a post-cookie world. It works because LiveRamp was neutral - nobody owned it, so everybody trusted it and used it.

That changes when Publicis owns it.

LiveRamp reported $813 million in revenue for fiscal year 2024, with 13% annual growth over five years and 107% customer retention (Digiday). Publicis paid $38.50 per share - a 29.8% premium to LiveRamp’s May 15 closing price - with total equity value of $2.546 billion including $379 million in net cash acquired (Publicis Groupe, 2026).

”Identity Is the Qualifier for AI”

Publicis CEO Arthur Sadoun framed the acquisition around a single thesis: “Identity is the qualifier for AI. If you don’t have the identity, you just don’t win with AI.”

The logic: when the entire market runs the same leading LLMs, differentiation doesn’t come from the model. It comes from the data you feed into agents - and critically, the ability to connect that data across platforms.

Publicis has been building this stack layer by layer:

- Epsilon (acquired 2019, $4.4B) - customer data and behavioral signals

- Lotame - post-cookie identity infrastructure

- LiveRamp - cross-ecosystem collaboration via RampID

Combined with Habu’s data clean room technology, this stack enables brands to activate data “without it ever leaving the owner’s hands.” A practical example Publicis illustrated: a bank’s AI agent integrating retail banking, credit card, and merchant travel data to cross-sell more effectively - while a competitor running the same LLM on generic data cannot replicate those results.

Publicis projects $50 million in cost savings in year one, and raised its 2027-2028 growth targets to +7% to +8% net revenue growth (Publicis Groupe, 2026).

The Neutrality Problem

The industry’s biggest concern isn’t the valuation. It’s what happens to LiveRamp’s “Switzerland” positioning.

LiveRamp CEO Scott Howe previously described the platform as “a neutral place where high-friction players come to resolve disputes.” With Publicis - direct competitor to WPP, Omnicom, IPG, and Dentsu - now owning it, the question is whether RampID can remain neutral infrastructure.

One data executive at a rival holding company told AdExchanger the acquisition is like “the referee joining one of the teams.” The historical pattern doesn’t favor Publicis: after acquiring Epsilon and Citrus, competing holding companies withdrew from both platforms.

Sadoun sent 500 personal emails to clients, partners, and competitors pledging four commitments: independent operations, open access with no client restrictions, full interoperability, and data used only with explicit consent.

A data point worth watching: LiveRamp’s direct customer count is already declining, from 900+ to 846 (AdExchanger). If that trend accelerates after the deal closes - expected before year-end 2026 - the market will deliver its own verdict on neutrality.

What This Means Beyond the US

Publicis operates directly in Vietnam through Leo Burnett, Starcom, MSL, and Saatchi & Saatchi. This deal has practical implications across Southeast Asia.

For brands working with Publicis agencies in the region: in theory, you gain access to improved data infrastructure. In practice, the question is whether your first-party data is clean and structured enough to benefit from it.

For brands not using Publicis: this is the clearest signal yet from global holding companies. First-party data isn’t a “nice to have” anymore - it’s the foundational competitive asset of the AI era. In markets like Vietnam, where most brands still rely on third-party cookie targeting and thin CRM exports, the gap between local data reality and global data infrastructure has never been more visible.

Tom Laband, CEO of Adsquare, put the existential question plainly: “In a world where AI agents plan, buy and optimize media autonomously, what is the agency actually for?” The convergent answer across the industry: whoever controls the intelligence layer - the identity data, the clean rooms, the cross-platform signal - controls the outcome.

The question isn’t which AI platform to use. It’s what data you own to make that platform work better than your competitor’s identical setup.

NateCue's Take

Everyone's debating which LLM is best. Publicis just bet $2.2B that's the wrong question. Models are commodity. When every agency runs GPT-5 or Claude Opus, differentiation won't come from the model - it'll come from what you feed it. Identity, behavioral signals, cross-platform data linkage. That's the actual moat. This matters beyond the US. From a Vietnam market perspective, most brands here still operate on third-party cookies and shallow CRM exports. The gap isn't about AI capability - it's about data readiness. The holding companies figured this out years ago. The LiveRamp acquisition is Publicis making it structurally permanent. The real question any marketer should ask today: what first-party data do you actually own, is it clean, and can you activate it cross-platform? If the answer isn't clear, the problem isn't your AI strategy - it's your data strategy.