Anthropic - the AI company that markets itself as the safe, responsible alternative to OpenAI and xAI - is paying Elon Musk’s company $1.25 billion a month. Not as part of an alignment strategy. Out of necessity.

The Competitor-Customer Paradox

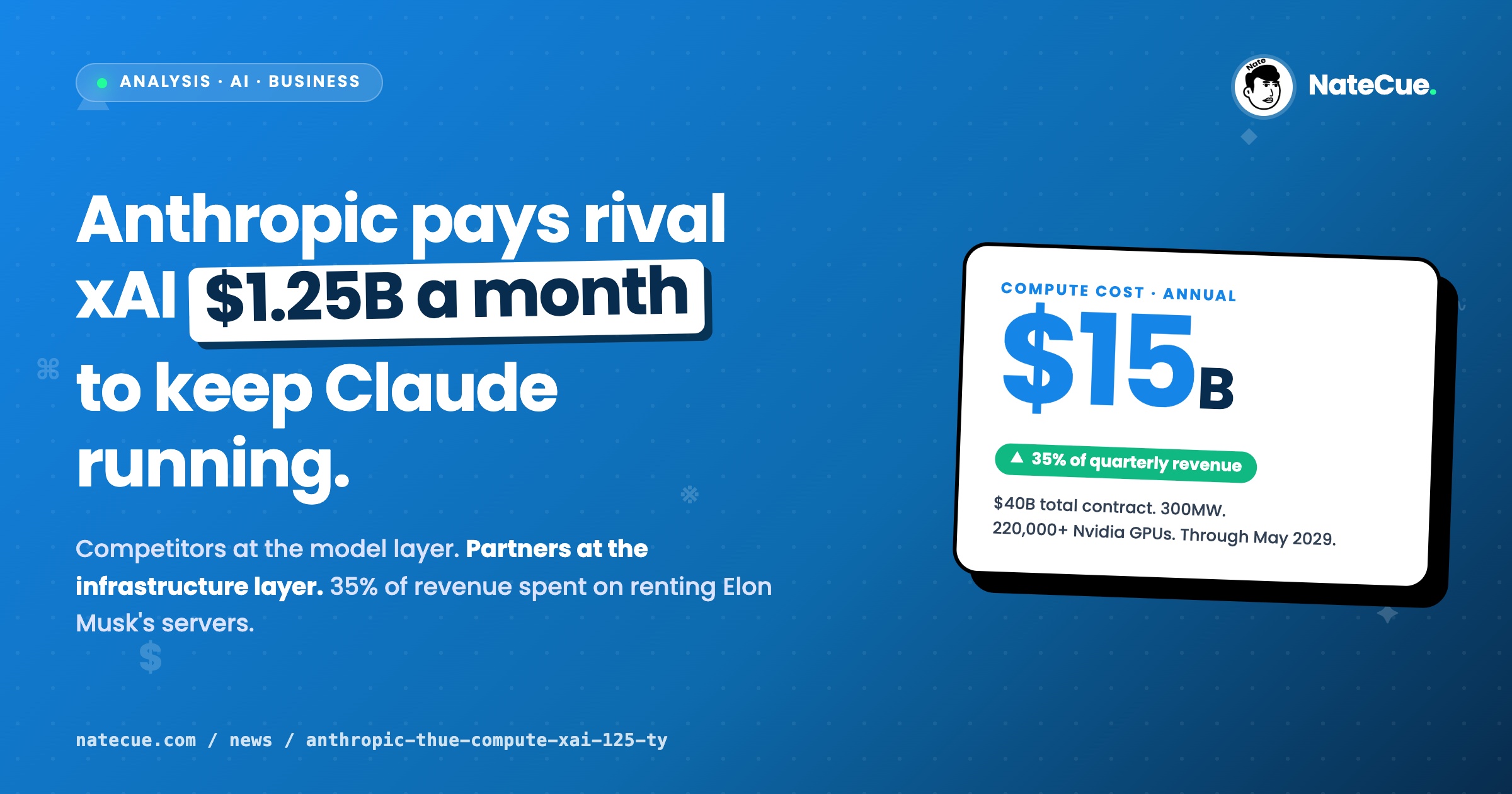

The deal was disclosed through SpaceX’s S-1 IPO filing. Anthropic rents the entire output of Colossus 1 - xAI’s Memphis, Tennessee data center - at 300 megawatts and 220,000+ Nvidia GPUs, through May 2029. Total contract value: over $40 billion (TechCrunch, 2026).

Shortly after, Google signed a separate deal with SpaceX at $920 million a month through June 2029. Between these two agreements, xAI is generating $26 billion in annualized compute revenue from two of its primary model-layer competitors.

The reason xAI has capacity to spare: Grok usage has dropped to an estimated 11% of Colossus 1’s capacity. A data center built to train and serve Grok now has more idle GPUs than its own models can use.

Compute Absorbs Revenue

Anthropic’s quarterly revenue runs approximately $10.9 billion (Enterprise DNA, 2026). The xAI contract costs $3.75 billion per quarter - roughly 35% of revenue going to infrastructure alone.

This is the actual cost structure of frontier AI. Not research. Not talent. Just electricity and hardware.

Analysts are calling this the “neocloud” model: AI companies that overbuild compute capacity, then monetize excess by selling it to competitors at the infrastructure layer - while competing head-on at the model layer. “The Anthropic-xAI arrangement illustrates what’s becoming normalized: competitors sharing infrastructure as a business necessity,” per TechCrunch (2026).

Google - which owns Gemini and competes directly with Claude - is in the same position, paying the same infrastructure provider. The model layer is a competition. The infrastructure layer is increasingly a shared dependency.

What This Means for AI Pricing

Compute costs are moving upstream. Alibaba Cloud raised prices 34% in June 2026 citing global GPU scarcity. Zylo’s 2026 SaaS Index found enterprise SaaS spend rose 8% year-over-year with no corresponding increase in the number of applications - meaning existing tools are simply costing more.

The pricing model shift is already underway: per-seat to usage-based. You pay per token, per API call, per agent run. As AI providers pass through infrastructure costs to customers, your 2027 AI budget could look significantly different from today’s estimate - especially if compute prices continue rising.

The 90-Day Clause Nobody Talks About

Both deals - Anthropic-xAI and Google-SpaceX - include 90-day termination clauses for either party.

If xAI needs Colossus 1 back - to train Grok 3, to serve a higher-paying customer, or for any reason - Anthropic has 90 days to find alternative capacity for 300 megawatts. That’s not a lot of runway when production systems are running on that infrastructure.

The contrast with South Korea is sharp: NAVER and NVIDIA are building gigawatt-scale AI factories domestically, starting at 55 megawatts in 2027. Sovereign AI compute is a real infrastructure strategy. Vietnam, most of Southeast Asia, and many emerging markets have no equivalent.

For enterprises in those markets building AI workflows on Claude or Gemini, this is a specific vendor dependency risk worth including in business continuity planning. The model you’re using is only as stable as the compute contract underneath it - and that contract has a 90-day exit door.

NateCue's Take

The 90-day exit clause buried in this deal is the most important detail nobody's discussing. Every enterprise workflow built on Claude today carries hidden counterparty risk: xAI can pull Anthropic's compute with 90 days' notice. For teams in markets like Vietnam and Southeast Asia - where no sovereign AI compute exists - this isn't theoretical. It's a vendor dependency gap that belongs in your business continuity plan now. The model layer will commoditize. The infrastructure layer is where concentration risk actually lives - and it's more fragile than the marketing suggests.