Last week, Anthropic committed $200 billion to Google Cloud over the next five years. The number is staggering. But it’s the structure of the deal - not just the size - that matters.

The $2 Trillion Circular Economy

Big Tech’s combined AI infrastructure capex in 2026: $650-725 billion. Amazon leads at $200B. Alphabet at $175-185B. Meta at $115-135B. Microsoft at $120B+ (CNBC, 2026). OpenAI has committed over $1 trillion in hardware and cloud agreements across the next decade (Built In, 2026).

The mechanics: Google invested $40 billion in Anthropic. Anthropic then committed $200 billion back to Google Cloud. That $40B investment becomes a $200B revenue backlog on Google’s books.

OpenAI mirrors this with Microsoft and Amazon. Total cloud revenue backlog across AI companies: $2 trillion (Engadget, 2026).

This isn’t organic revenue growth. It’s circular capital - Big Tech investing in AI startups that contractually commit those funds back to the same cloud infrastructure. The result is impressive-looking backlogs that are, at their core, money flowing in a loop.

Analysts at Futurum Group (2026) warn that Big Tech free cash flow could fall by as much as 90% in 2026 as capex outpaces real revenue growth.

Why Anthropic Needs This Much Compute

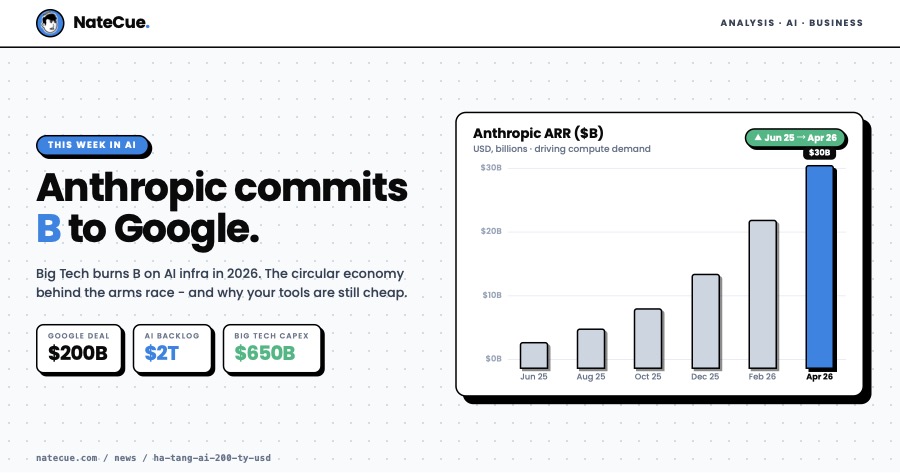

Anthropic’s server costs are projected to hit $20 billion in 2026 alone (Engadget, 2026). Annual recurring revenue has passed $30 billion - but compute costs scale at the same rate.

The $200B Google deal centers on TPU (tensor processing unit) capacity starting from 2027. Anthropic has also signed separate deals with CoreWeave and Amazon to diversify compute supply.

TechCrunch (May 2026) reports Anthropic is simultaneously launching an enterprise joint venture backed by Blackstone and Goldman Sachs, with forward-deployed engineers embedding Claude into existing workflows at hospitals and enterprises. More enterprise customers means more inference demand, which requires more compute.

The underlying dynamic is simple: each generation of frontier AI model costs 10-100x more to train than its predecessor. Compute isn’t infrastructure - it’s the primary competitive moat. No compute, no model. No model, no revenue.

What This Means for Southeast Asia

Two signals worth noting for emerging markets.

First: Vietnam has attracted more than $7 billion in AI data center investments over the past six months (ERP Today, 2026). Google has announced plans for a hyperscale data center in Ho Chi Minh City, expected online by 2027.

Second: Southeast Asia’s data center capacity is forecast to grow 20% annually through 2028, with total market size exceeding $30 billion by 2030 (Southeast Asia Data Center Landscape Report, 2026). The region is becoming a serious infrastructure hub, not just a consumption market.

For marketers in Vietnam and the broader region: API latency from Southeast Asia will drop meaningfully post-2027. Access to Claude, Gemini, and GPT-5 will become faster and more reliable. That’s the technical story.

The strategic story is more interesting.

The Subsidized Window - And When It Closes

Right now, marketers everywhere are using AI at prices far below the true compute cost.

ChatGPT Plus at $20/month. Claude Pro at $20/month. Gemini Advanced bundled into Google One. API tiers priced to drive adoption, not profit.

This is intentional. Big Tech is absorbing losses to build workflow dependency - to make switching painful before the monetization phase begins.

The $200B Anthropic-Google deal is a signal that this subsidy phase is at its most intense. The arms race is at its peak. The “burn money to win the market” playbook is running at full scale.

But no subsidy phase lasts indefinitely.

When Anthropic needs to show returns to Blackstone and Goldman Sachs - or when its IPO arrives - pricing will rationalize. API costs will rise. Consumer tiers may narrow. Enterprise contracts will take priority over cheap access.

This isn’t a prediction. It’s how every platform cycle has ended: subsidized growth, dependency lock-in, monetization.

The question is timing. Not whether.

Until then: marketers are in the best possible window to experiment, build, and embed AI into their workflows. Not because AI is magic. Because Big Tech is effectively subsidizing your education in using tools they plan to monetize later.

The infrastructure arms race is real. The beneficiaries, for now, are us.

NateCue's Take

The $200B Anthropic-Google deal isn't just a cloud contract - it's a window into where we are in the AI cycle. Google invests $40B in Anthropic; Anthropic commits $200B back. OpenAI mirrors this with Microsoft. The $2 trillion revenue backlog looks impressive on paper, but it's circular capital, not organic growth. For marketers, this has one practical implication: the cheap AI access you're getting right now - $20/month for Claude Pro, near-zero API costs - is a subsidized land-grab. Big Tech is paying for your workflow dependency before monetizing it. When Anthropic IPOs and Blackstone needs returns, pricing will rationalize. The window to experiment cheaply is finite. Build your dependency on the tools that matter, now.